Brexit seems to mean “sterling crisis” – but does it mean a trip to the IMF as well?

Britain is used to “lights out” humor. But today seems different. In the UK, there are clear parallels with the 1970s, a decade that saw the country enter Europe, confirm it with a referendum, and then seek an IMF bailout. In this longer post we explore those parallels, and consider a subset of the risks, pertaining to the external position. We didn’t like what we saw.

Oh how good we had it in the seventies

Some may know that back in the 1970’s, the UK was flirting with Europe, badly managed by inept political parties, themselves riven with divide, the Pound meant something, and the UK ended up going to the IMF. In this post, we discuss the similarities, and ask that vital question – will the fate be the same?

Some may know that the UK joined the EEC (as then) back in 1973. Some may even know (or be confused by the fact that) the UK had a referendum in 1975 to confirm its membership.

Some will also know that within a year, the UK was going cap in hand to the IMF for (close to ) $4bn.

For those with a thirst, please read through those links above. Our desire here today is to understand the lessons of that history, not evaluate the mistakes made. For one, we don’t have an enormous oil shock (1973) to deal with. That hopefully will prevent us dusting off that most 70s of phrases “stagflation”.

Capital flows – but both ways.

Some have in the past likened the UK economy to a hedge fund.

She has domestic assets, especially property, but she uses them to leverage her wealth, by borrowing abroad, in foreign currency, to buy more assets abroad.

Some even suggest the perennial current account deficit is involuntary. The UK doesn’t actually want to buy all those German cars and French wines. She has to. As the capital account is bloated by all the income from those foreign assets, coupled with the voluntary foreign capital that flows into UK “safe houses” and “critical” technologies and companies, the cars and wine just have to flow to balance the tautology. Ooh, if you must…

We’ve always had some sympathy for that view. Indeed we see the US in much the same way, especially during the 90s when she was THE emerging economy. But that’s for another day/post.

So what’s the prospect for that capital ebb and flow today? Well according to the BoE, not so good.

The devil is in the detail

This is how a good friend described it to me today.

“Remember – this could be very key in 2019 – BOE Financial Stability report: The ability of the UK to refinance its large stock of external liabilities and to fund its current account deficit is affected by overseas investors’ willingness to continue to hold UK assets. Sharp falls in foreign investor appetite for UK assets could lead to falls in UK asset prices and a tightening in domestic credit conditions. This could be triggered, for example, by perceptions of weaker or more uncertain UK long-term growth prospects.

If you missed it earlier in my note:

CBRE reported that commercial values and rents, both fall for first time in six years!

BOE Stability report in the current account section:

Foreign investor transactions in UK CRE from the United States and Asia, accounted for 50% of transactions in UK CRE in 2018 Q2. So CRE flows matter!

Deterioration in energy, base metals and now equity markets does not bode well for foreign corporate receipts and Sterling since June has not been weak enough to offset losses in the current account.

As I noted at the weekend – the collapse in M4 and amount of capital likely to be leaving the UK into Europe for banking businesses given current confidence that capital shift, will be potentially massive.”

Let’s look at each of these point in turn.

How sound is UK commercial real estate ?

The first point is that rents and capital values are declining for the first time in six years. Well yes, even the Royal Institute of Chartered Surveyors ( RICs ) survey out last month pointed to weak commercial real estate (CRE), although focused in retail where “amazonifocation” continues relentlessly. The weakness was patchy, but shows up clearly in both the text and the charts.

“At the all-sector level, respondents left near term rental expectations unaltered, with the national reading remaining at -2%. As such, this points to virtually no change in headline rents over the coming three months. On a twelve month view, both prime and secondary industrial rents are envisaged posting solid growth, with expectations moderately positive for prime offices. On the same basis, secondary office rental projections are broadly flat. Expectations remain firmly negative for retail rental levels over the coming twelve months, both in terms of prime and secondary space.”

The charts below show the clear weakening in rents and values, but it’s heavily focused in retail. Even secondary offices are making a comeback on a 12 month basis, but that’s at the expense of valuations. And overall office rents look very soggy.

From the BOE Financial Stability Report (FSR p 40)

“In the UK commercial real estate (CRE) market, foreign investors, notably from the United States and Asia, accounted for nearly 50% of transactions, and 71% of London transactions, in the 12 months to 2018 Q3 (Chart E.3).

The leveraged loanmarket is also particularly reliant on cross-border investment. 85% of the total gross issuance of leveraged loans by UK non-financial companies was syndicated abroad in 2017, a record level. This share increased to 94% in the year to November 2018 (Chart E.4).”

But perversely, therein lies the good news ;

“There have been substantial foreign capital inflows in the past two years, affecting various sectors…

Over the period 2012–15, the current account deficit was financed by UK investors selling overseas assets at a faster rate than foreign investors were selling UK assets.

However, this position has reversed since 2016, and foreign inflows have been substantial (Chart E.2). A material share of these inflows since 2016 has been in the ‘other investment’ category (Chart E.2). This includes inflows of loans and deposits to banks, which can be short term in nature and hence subject to refinancing risk.

Unlike the period before the crisis, though, the UK banking system currently has more foreign assets than foreign liabilities.”

The good news is on the last line. Yep “UK llc” has loads of foreign assets, much of which is in the banking sector, despite all the selling previously.

”Major UK banks were resilient to the external financing risks in the 2018 stress test.

In the event of a material reduction in foreign investors’ appetite for UK assets, there are several factors mitigating risks to the UK banking system and the broader economy.

UK banks have strong liquidity positions, including on a foreign currency basis. And at an aggregate level, UK residents hold more foreign currency assets than liabilities. This mitigates the economic risks associated with currency depreciation.”

So again we see that even the banking system loves a weaker sterling.

So why should sterling fall if this is such good news ?

Well sterling is likely to fall as capital outflows hit home in multiple ways.

Firstly the foreigner will hedge their sterling risk. That’s precisely what we’re likely seeing now. Then we’ll see actual disposal of assets, which takes time. A long time. Look out for the disposals on the usual CRE websites and news services.

Finally there will be unrelated but second order “panic hedging” of Sterling by other “investors”. That will mark the low in both the currency and the panic.

As the BoE note, the fx markets already smell blood..

So let’s look at the next point.

Money money money

Has UK broad money growth really been slowing, and if so, so what?

Well The Telegraph has noticed. BTW, what is M4ex? – M4ex is standard M4 less intermediate OFCs. It’s broad money supply but takes account of double counting from the “shadow banking system”. It was the clearest signal that we were headed for the GFC back in 2006, and the BoE wrote about the risk in its reports back then.

And yes it is slowing, in that it’s growing more slowly, as the excellent Simon Ward at JanusHenderson points out here (brown line)

And note also its growth rate in 2006…

But don’t worry – how many times do you think M4ex, or for that matter, “money” appears in the latest BoE Inflation Report ? Yep – none (the word “money” appears, but refers to “out of the Money puts options”).

Even in the minutes of the last Policy meeting, the word money appears but twice, and one of those is in the title “money, credit, demand and output”, pertaining to a segment which does not discuss money even once. Perhaps re-name it “Credit, demand and output”?

No, put plainly, the BoE could care less about the money aggregates – Tom Congdon tear your hair out!

The regularity of regulation

My friend’s final point was that capital will leave the banking system as Brexit draws near. This is certainly supported by recent comments from regulators regarding the need to capitalize overseas (aka EU now) operations separately.

It’s hard to imagine Barclays for example, reigning in her foreign operations, nor for that matter, moving outside the UK. No she’ll put more capital (or business) overseas.

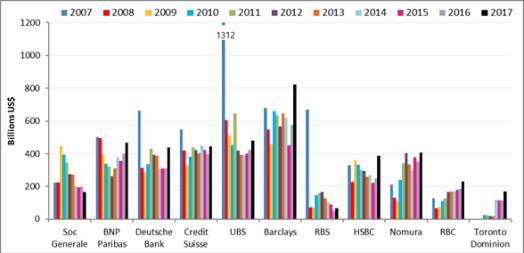

The BoE notes above, that UK banks have a strong liquidity position, including in foreign currency. Perhaps that’s why even as recently as 2017, Barclays stands out on a collateral basis, from its European peers.

Pledged Collateral Received by European and international banks (Billions of US$) Source : Singh and Alam – Collateral velocity rebounds

”The Bank has also reviewed banks’ exposures to large listed UK companies, which have become more highly indebted over the past year. The proportion of debt owed by large listed UK companies with a ratio of net debt to EBITDA greater than four increased from 31% to 38% between the 2017 and 2018 stress tests. But the proportion of stress-test participants’ exposures accounted for by these riskier firms has remained stable, at around 13% (Chart F.11).

Major UK banks have not been the main providers of debt to these companies.

The FPC and PRC continue to monitor closely the underwriting standards of UK banks originating leveraged loans. The FPC will continue to review how pockets of corporate indebtedness in the UK, and the increasing role of non-bank lenders globally, could pose risks to UK financial stability.”

But of course, the Bank has stress tested these exposures – from a UK bank perspective – and feel it’s ok. One hopes the other regulators have stress tested their banks for as deep a Brexit disaster scenario as the BoE. They also need to consider the second order impact on these “large listed UK corporates, especially where the debt is in (appreciating) foreign currency. So expect UK plc hedging those foreign currency liabilities.

Will the last sterling holder please turn the lights out

So, it’s plain to see where the hedging of Sterling assets, and the capital outflow, will (are? ) coming from. The fact that sterling is facing the brunt of the Brexit uncertainty should be no surprise.

But will history repeat, or even rhyme? Will we see a UK Chancellor go cap in hand to the IMF?

No one can know for sure, and we’ve certainly no IMF’n clue, but as we can see from the above analysis, while the “UK llc hedge fund” benefits enormously (as a whole) from the fall in sterling, as those foreign assets appreciate, there is a limit to the UK banking sector’s capitalization and health, and while the BoE stress test looks more than adequate to cover the first order effects of a “bad Brexit”, there is surely a matrix of sterling exchange rates that test that solvency in the second order.

Unless the UK economy speeds up sharply, and CRE recovers quickly, Sterling looks set for weakness whatever the Brexit outcome.

That said, a “bad Brexit” would extend and hasten those losses.

Selling England by the pound

To conclude, get ready to hear the phrase “parity party” a lot as we head towards party season, but be sure to ask, is that against the US$ or the Euro?

The history of sterling/dollar 1985 to today Source – tradermade

If you want to talk to my friend about this, drop me an email.

Semper Fi.

NB – these are the (inflated) opinions of the author, and are NOT investment advice.