In this post, the second of a series of posts addressing the end of Libor and her relatives, we look at what’s being proposed to replace these key benchmarks. In future posts we’ll discuss how this will impact financial markets.

Light is starting to emerge from the tunnel – is it an alternative benchmark?

By acting now, the FCA is harnessing the energies already at work to attempt to reach a smooth resolution. In requiring banks to continue submitting rates until end-2021 the prospects for a smooth transition are good. However, herein comes thefirst problem – will legal and compliance officers take the line that to continue to submit rates to a market that is dying, becoming less liquid (with consequently fewer trades to validate submissions) and still fathering lawsuits, amounts to an unnecessary legal business risk and call a premature halt themselves. While the FCA always has significant “moral suasion” facilities to persuade panel banks to continue to submit, their formal authority to compel banks expires in 2020 under the new EU benchmark governance rules entering force in 2018. As FCA Chair Bailey explained in his 2017 speech, the risk of an avalanche of departures is a real one.

This risk obviously warrants the swift adoption of a replacement benchmark. Herein lies the second problem. In all five currency regimes, there is still no formal agreement on a precise replacement for LIBOR. To elaborate that point, we look at what the US is doing, then contrast with other regulatory regimes.

The US approach – a case study – Secured Overnight Financing Rate (SOFR)

In the US, regulators have promised to publish three new reference rates from early next year, one of which has been endorsed by a US-Based working group called the Alternative Reference Rates Committee (ARRC), the Federal Reserve Board and the Federal Reserve Bank of New York. That rate, the Secured Overnight Financing Rate (SOFR),is the strongest contender, backed by transactions including tri-party repo data from the Bank of New York Mellon, and cleared bilateral and GCF repo data from the Depository Trust & Clearing Corp. (DTCC). Outlier transactions, where the collateral is “special”, will likely be excluded, leaving plenty of transactions which could amount to $600-800bn in daily value, ensuring “transactional validity” of the rates. The other two proposals, the Tri-party General Collateral Rate (TGCR) and the Broad General Collateral Rate (BGCR) would cover a subset of these transactions. Note, initially the rate was called the BTFR (Broad Treasury Funding Rate), but the Fed has since re-christened it SOFR.

The Fed and US Treasury have promised to post rates based upon these three benchmarks. The SOFR rate will have some volatility, but overall could provide a solid, transaction-based benchmark. However, importantly the SOFR does not yet exist, and the lack of trading remains a problem. Once it’s posted, markets will be encouraged to utilize it, and as such it clearly has potential to become the benchmark for USD liabilities. . While not formally published, the Fed has been keeping track of the benchmarks, and Exhibit 2 shows the recent behavior of the SOFR/BTFR rate, plus three different proposals considered by the ARRC, as detailed fully in their June 2017 materials.

The stability of all the proposed alternative US$ LIBOR rates, generally trading between the Fed’s IOER and overnight repo rates, supports their potential for consideration as replacements for LIBOR.

Exhibit 2: The Recent Behavior of Alternative Benchmark Suggestions

Source: The Alternative Reference Rates Committee – June 16, 2017

We’re now entering the market consultation phase in most of these markets. In the US the Federal Reserve have given the industry 60 days to provide comment, leaving an ample 6 months from November to April to make adjustments before they begin to post . With the debt ceiling issue still to be fully resolved, the delay may be fortuitous, avoiding any volatility in repo rates which may have tarnished SOFR in its early stages, and damaged its chances of successful adoption

What are others doing, and is there any consistency?

In other regulatory regimes, there are signs of consistency, but there has also been some fragmentation. In the UK, the Bank of England has suggested switching to SONIA (Sterling Overnight Index Average – a swap rate at which interest is paid on sterling short-term overnight wholesale funds in circumstances where credit, liquidity and other risks are minimal) an OIS-based rate that is also unsecured, and is still subject to its own reform process independent of LIBOR. The reformed SONIA will soon be up and running, with full transactional backing and validity, and the support and encouragement of the BoE.

We discussed above the approach being take in Europe, and it seems the attempt to reform EURIBOR retains the ambition of keeping EURIBOR alive in spirit, in the form of a “hybrid”. But the final choice for accompaniment to EURIBOR, in the form of EONIA and the new ECB rate, remains to be settled.

Each of the other major regimes is proceeding in its own direction. In Japan, where JPY-LIBOR amounts to USD30trn of exposure, working groups seems to have settled on an unsecured Tokyo OverNight Average (call) Rate, TONAR.

Alternatively, the Swiss have decided to replace their unsecured OIS-based benchmark TOIS (not LIBOR-related) with a new secured repo-based benchmark, SARON from the end of 2017, from which participants should move to the new SARON rate, or terminate the existing contracts, as the old TOIS rate will no longer exist. This may offer some guidance on the challenges of the proposed LIBOR transition. It also points to the need to set a timetable for LIBOR, as Bailey mentioned in his speech. “In Switzerland, for instance, it has been clear for some time that the TOIS reference rate would not survive. But only once a date was agreed for its discontinuation – 29th December this year – did serious work on transition to the new reference rate, SARON, begin.”

So, while there is clear fragmentation between regulators, and multiple choices appear alive within each currency regime, the momentum and support of key bodies like the Fed and BoE offer some optimism.

Some key challenges of starting with overnight rates as benchmarks.

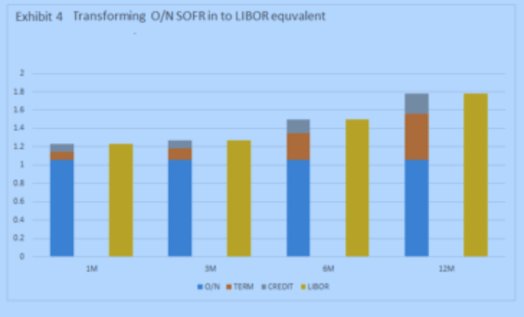

One commonality between choices across all five currency regimes is the fact that they are all based upon overnight rates. This presents the third major problem – how to turn an overnight rate (like SOFR) into a term rate (like 3mth LIBOR).The current market discussion centers on applying a fixed, ad hoc “term spread” for each maturity up to 12 months. Precisely how to calculate it is unclear. Guidance from existing term GC repo markets may help. This term valuation metric is expected to evolve with a transition period, during which participants could use “hybrid” models to value and mark to market. But eventually a formal market in the term dates will have to evolve to facilitate valid marking to market across the full maturity spectrum. Even after the term markets evolve, it’s likely that the bulk of volume will occur in the overnight SOFR/BTFR, declining further down the maturity spectrum. This will be a key difference from LIBOR where the most popular term has always been the 3 month.

Finally, and related to the term premium issue, comes the fourth problem with all the proposed replacements – the lack of credit risk, a hallmark of the LIBOR rates which were designed to reflect bank unsecured credit risks.All of the proposed benchmarks, be they secured or unsecured, have been chosen as “risk free rates” (RFRs) and as such, is expected to carry minimal credit risk. This translates into significantly lower rates than LIBOR, even in calmer times. The use of these rates as a discount factor for derivative transactions, or as a surrogate for AA-rated yields used to discount pension liabilities, will result in much higher valuations than using LIBOR based rates. This will cause “ad hoc economic transfers when the switch is ultimately made to an alternative benchmark rate” and must be avoided if the transition is to take place smoothly without recourse to combative legal action. Again, the solution appears to be another ad hoc “credit spread“ added to the overnight rate, adjusted for term premium.

The same questions of fairness and calculation method arise.

Exhibit 4 demonstrates how this will work.

In exhibit 3 we tabulate for each major currency regime, the likely choices for replacement rate and their pros and cons.

Exhibit 3 – Summary of alternatives and transition plans

| Interest rate

Bench-marks

|

Size

USD trn Appx. |

% roll-off in 5 yrs | Proposed

Alternative Footnote 1 |

Prospects

for success / Phase |

Positives | Concerns |

| $ LIBOR | $150+ | 76% | SOFR/ BTFR

Secured o/n |

Fair /

Consul-tation |

Based upon $600b+

transactions |

O/N rate, No method for Term and credit premium

|

| GBP LIBOR | $30 | 68% | SONIA-link OIS Unsecured o/n rate | Fair /

Consul-tation |

GBP SONIA well established, already $8trn+ market | Still unsecured rate, and SONIA in process of reform itself. No method for Term and credit premium

|

| EURIBOR | $200+ | 68% | “Hybrid” – ECB Unsecured o/n rate | Unknown / research phase | Timetable allows for research through 2018

Implemen-tation 2019. ECB announce-ment |

Reform is failing, Panel desertions – ECB/EONIA o/n rates – no term/ credit premium

|

| SFC LIBOR & TOIS | $6+ | 71%

|

SARON

(secured) o/n rate |

Fair /

End 2017 implemen-tation

|

Strong regulatory guidance, small market | Short timeframe for implementation |

| Yen-LIBOR

& TIBOR |

$32+ | N/A | TONAR

Unsecured o/n rate |

Good / propose

/review |

Initial consultation favorable, backed by Yen 3-4trn transactions | Reliant on “tansi” brokers |

Footnote [1] In the UK, the Bank of England has suggested switching to SONIA [1]an OIS-based rate that is also unsecured, and is still subject to its own reform process independent of LIBOR. The other major market, Japan, JPY-LIBOR amounts to USD30trn of exposure, and working groups have settled on an unsecured Tokyo OverNight Average (call) Rate, TONAR. [1] Alternatively the Swiss have decided to replace their unsecured OIS-based benchmark TOIS (not LIBOR-related) with a new secured repo-based benchmark, SARON from the end of 2017, [1]from which participants should move to the new SARON rate, or terminate the existing contracts, as the old TOIS rate will no longer exist.

Source: MPG 2014, BoJ, Authors calculations

Europe – EURIBOR, EUR-LIBOR, EONIA, EURONIA, and now a new ECB overnight rate?

The evolution of financial markets can never be linear and straight forward. The competition from different countries, and in some cases, financial centres within countries, always leads to multiple examples of (largely) the same market. No less the case with European money markets. Once the Euro currency was formed, European regulators attempted to wrestle the euro-denominated (and not to be confused with the Euromarkets of the 1980s) financial markets from the hands of London and other financial centres. The EURIBOR and EONIA markets are the basis for that attempt. EURIBOR, as discussed above, is the European answer to LIBOR,a panel-based unsecured interbank lending market, using EU-based banks. The overnight equivalent is EONIA, where banks deposit funds unsecured. Both rates are index-averages of panel bank submissions, with all panel members either based in the Euro area, or non-EU international banks with substantial eur-currency businesses.

EURIBORhas long been the biggest competing benchmark to LIBOR, and has now become, together with EONIA, the market where Eurozone banks offerto lend unsecured EURO funds to other banks in the interbank market. EURIBOR is outside the remit of the FCA, LIBORs regulator, instead administered by the European Money Markets Institute (EMMI).Having successfully absorbed the Euro-LIBOR market which has largely disappeared, EURIBOR is huge. Comparable numbers for the exposure to EURIBOR benchmarks was around USD 220 Trillion in 2012. EURIBOR, being an unsecured benchmark, has also suffered from minimal transactions and panel bank defections. To that end, it is equally flawed.

Following the LIBOR manipulation scandals, the EU crafted new benchmark regulations, which come into applications from Jan 1st2018.[1] In May 2017, the EMMI announced that their previous attempt to move EURIBOR to a transactions-based rate had failed and they would seek “hybrid” solutions.

One thing the Euro- system doesn’t need, is another acronym attached to a benchmark interest rate. So the ECB decided to create their own overnight unsecured rate, announced in September 2017, to be administered by themselves, using transaction and quote data they collect, and to be fully functioning by 2020. It will appear to many that the only difference from EONIA is the fact that this is a public-sector version while EONIA is fully private sector. In reality there are a number of key differences which will ultimately decide its eventual success. Firstly it will take most (actual lending) transactions into account, rather than a single panel submission from each bank, as EONIA (and EURIBOR) do currently. Secondly it will (potentially) cover a larger universe of submitting banks. EONIA was intended to use submissions from its panel of up to 28 panel banks, while EURIBOR employs 20 banks on its panel. The ECB now requires over 50 reporting agents to provide data on a vast number of lending transactions through its Money Market Statistical Reporting (MMSR) program. The new rate will includes fx swaps and Overnight Index Swaps (OIS), together with lending transactions with non-EU entities. By employing a broader universe than EURIBOR and EONIA, it’s thought to guarantee the transactions for all maturities on every reporting date. Recall, these are still unsecured transactions, of which there has been too few to enable EURIBOR rates to claim transactional validity and backing.

For completeness, EURONIA is the London-based index average of interest rates on unsecured overnight euro deposits arranged by eight money brokers in London. It is thus a London-based equivalent of EONIA, the overnight equivalent of EUR-LIBOR.

As we saw above, the EURIBOR and EONIA markets have come to dominate their London-based competitors, EUR-LIBOR and EURONIA. However all four rates trade, and appeal to a different segment of investors and borrowers of Euros.

The new ECB overnight rate (let’s call it ECB-ONIA for fun) is yet a fifth version of an unsecured benchmark rate. The reason the ECB opted to create a new overnight rate rather than reform the existing EONIA rate (as the UK Bank of England has done with reformed SONIA) is unclear. Indeed, it’s possible the ECB will “back” the new rate into the EONIA system, and hand over administration to the EMMI (who are responsible for EONIA), once it’s established. But either way it’s hard to see both ECB-ONIA and EONIA both coexisting in the medium term.

However, it is possible we could end up with three (EURIBOR, EONIA and ECB-ONIA) weak and ineffective benchmarks. In sum, the EURIBOR reforms may be floundering too. So, in addition to the LIBOR challenges, we find EURIBOR in disarray. Together, it’s estimated that the LIBOR and EURIBOR markets impact between USD360-600 Trillion of securities. This remarkable number embodies the size of the challenge faced by the World’s regulators and the financial markets they serve.

EONIA reform – following the path the BoE is taking, towards a EURIBOR replacement?

As discussed above, we can see some similarities with the path taken by the UK authorities, in creating a “risk free” overnight unsecured benchmark as the basis for their replacement of LIBOR. By increasing the amount of transactions included in their reformed SONIA rate, they are more likely to be able to satisfy the “transactional validity” requirement of a strong benchmark.

This is likely the strategy of the ECB with their new ECB-ONIA rate. The existing EONIA overnight rate was once a solid benchmark, with substantial transactions and a thriving derivative market. However, more recently, transactional volumes have fallen as Exhibit 4 shows. There are doubles several reasons for EONIAs decline, but Partly the cost of the ECB’s monetary easing, with first the LTRO loans in 2012, and then the TLTRO and QE programs each taking a chunk out of the EONIA market.

Exhibit 4

Source ECB

On one day in June 2017, volumes fell below a billion euros. And with the ECB QE program likely to continue to grow into 2018, it’s clear EONIA will not provide sufficient transactional backing for many years. Hence the ECB action to create a competitor alongside.

How big is the challenge of replacing EURIBOR and EONIA?

EURIBOR and EONIA areused as a reference rate in both cash and derivative markets and stand at the centre of the EU banking system. As well as use in financial contracts, it is also often the reference rate in late payment clauses in commercial contracts, and the benchmark rate for money market funds and asset management strategies.

EURIBOR is the basis for estimating funding, and therefore the valuation, of the majority of EU debt securities, either explicitly (interest paid tied to EURIBOR) or implicitly (using EURIBOR to determine the financing of non-EURIBOR-related securities). More conservatively, using largely 2012 data from the Market Participants Group (MPG) on Reforming Interest Rate Benchmarks, 2014, the direct exposure to EURIBOR is approximately US$223.6trn, (against around $152 trillion in US$ LIBOR), ranging from syndicated and mortgage loans to securitizations and of course derivatives (See the RODNE paper for more details). The MPG report also estimated the average roll-off periodsfor the various asset classes, which may give one an idea of how much of this exposure will have naturally rolled off before the proposed end date for LIBOR. For example, 90% of syndicated loans were expected to roll off within 5yrs of 2012. Therefore we can expect a large portion of syndicated loans to be “naturally” renegotiated before the 2021 date, perhaps to a new benchmark rate, were one to exist. Conservatively, we can estimate that 68% of the US$223.6trn will have rolled off within 5 years,and as such, can be renegotiated naturally within the 2021 deadline. Similarly, taking the ECB’s lead, other regulators could employ moral suasion” to help the migration.

Therefore we should expect that the ECB will work towards reforming and transitioning the EURIBOR markets towards fresh new benchmarks as the UK FCA follows through with their intent,sometime around 2021, perhaps with a short delay, to have retired LIBOR.

So where does that leave the EURIBOR replacement?

On the 21st September the ECB and European Commission, alongside the Financial Services and Markets Authority (FSMA), and the European Securities and Markets Authority (ESMA, launched a new working group to accelerate the already in-motion program of developing a “risk-free overnight rate which can serve as a basis for an alternative to current benchmarks used in a variety of financial instruments and contracts in the euro area” – essentially a “hybrid” solution to EURIBOR. While entirely speculative on our part, it seems plausible that the intent is to grow the “hybrid solution” out of the new ECB-ONIA overnight rate, in much the same way the UK will grow the LIBOR term replacements out of the reformed SONIA. They have set a target of 2020 to have it up and running – convenient for the FCA’s target to remove LIBOR by end-2021.

2 Replies to “LIBOR / RODNE Part 2 – The Fixes”