Our new weekly post – all our comments and views summarized and reviewed on a Monday morning.

Slightly reduced notes this week in honor of the holidays.

That was the week that was

Brexit – Corbyn foot in mouth

Little to add on Brexit (you’ll be relieved to hear). We wrote here and here how we saw the developments, and can only see the camps either backed into corners (UK participants) or waiting for the UK opposition to finish making mistakes (The EU).

The fiasco with “lip reading” seems well judged if it was intended to deflect from the actual verbal disasters made ( calling no confidence motions then retracting them). All that’s left is to see if Corbyn can get both feet in between those readable lips.

We’ve not changed our minds – 85% #MeRef2 – 15% #NoDealArmadegginouttahere

Stocks – I can’ney bear it

The S&P 500 closed the week down 7 percent and is just 16 points away from a key support level of 2,400. It is also just about 2 percentage points from a bear market.

The Nasdaq dragged down by tech and biotech is now the first index to close in bear market territory today. It lost 8.4 percent to 6,332 in this past week.

The Dow fell 6.9 percent this week to 22,445, and is just 3 percentage points away from bear market territory, or a 20 percent decline.

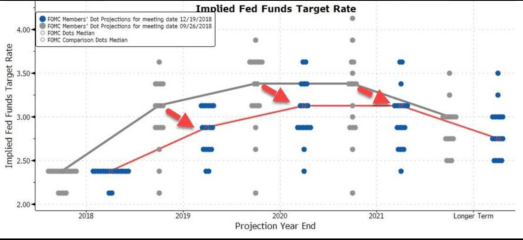

Markets were calm, treading water until Wednesday, when the Fed planted a land mine and the market trod on it. We don’t have a lot to add on the Fed, feeling that this chart says it all, and is consistent with our view that they are moments from “pause”, and will dress that up with “intent to hike a couple more times” for as long as they can – “ Pause with a bias to tighten” is the mantra.

The rest of the weeks was made up of turning noises into loud bangs, to which, markets have become vulnerable.

One of the loudest was the “apparent threat” by POTUS to fire Fed Chair Powell. As if to enhance the point, POTUS and Congress failed to agree on a spending bill and the Government duly shutdown.

Then, this evening, as if to add comedy to the calamity, Treasury Sec Mnuchin tweeted from Cabo, Mexico, that he’d spoken to all six SIFI bank CEOs and all was well. Mass media immediately dusted off the typical rhetoric of “shouting fire in a cinema” and laced with pictures of Jimmy Stewart trying to calm bank customers in “Its a wonderful life” the damage was done. Markets are set for a calamitous opening, without Asia to take the lead.

The VIX took its cue….

What’s our take ?

Trouble in Trumpton

Well it’s complicated. Firstly to see the POTUS talking of firing the independent Fed Chair he himself appointed, would be terrible for markets.

So to see Mnuchin come to his defense and deny this talk makes sense and in normal times, would have been the end of the matter.

But we’re not in normal times. And as such, it only stokes the fire.

But the real damage is being done off (the financial) stage, with yet more resignations and “firings”. Having seen Kelly “retired” to see SecDef Mattis sent packing earlier than his resignation letter requested, reminds us that this Administration is in danger of collapse. It’s not there yet, but it has the turnover of an Amazon warehouse at Christmas.

Then there is the statement from SecTres Mnuchin from Cabo. Again in normal times this would have been kept secret, only “rumored” to signal to those not on the call, but in need-to-know status. The masses would sleep easy in their beds, and talk of “puts and plunge-protection” would soothe the foreigner.

So why did he do it? We obviously can only guess, but this is the way we saw it.

Everyone has come across an administrator during their career, usually straight out of “consultancy”, armed with the McKinsey “tablets”, who knows how to spread the blame, share the responsibility, and who’s only means of leadership is to “bring you into the circle”. In other words, rather than actually want your opinion on something, they call a meeting and have everyone say their piece, knowing full well that no one will show any dissent. Then after the meeting, “we’re all on board”. The dissent goes on in the shadows, but if the plan fails and there is blame to apportion, no one can say “I told you so”.

Could this be the simple reasoning for such calls and meetings between senior bankers, regulators and such?

But for all that “politicking”, Mnuchin made a valid point – having this Powell-spat spoil “his trade deal to end all deals” seems counterproductive –

China

Which naturally brings us to China and trade wars. In short “Going swimmingly”

But on the other side of the ledger…

And a couple of interesting reads on Huawei and the medium term –

https://asia.nikkei.com/Opinion/Huawei-affair-growing-Communist-Party-role-in-China-s-big-tech

Europe

Apart from the Brexit buzz, very little caught my eye Re: Europe – with the exception of this – Hat-tip Matt Kessell (check out his posts on LinkedIn).

Our conclusions – beware.

This chart remains the worry –

So far we’re repeating the 1987 pattern, albeit more slowly. To end up down 20-30% from the highs, but over weeks rather than in a single day, seems more “boiling frog” than “better”.

Christmas Book list

With one day to go before Santa, it’s probably too late to ask the loved ones for these, but in case there are book tokens in the stocking, these might come in handy;

What I’ve been giving my friends…

And if you really must dwell on the wonderful life…

Which gives me a chance to plug one of my all-time favorite books….

Semper fi until next week. – Have a wonderful holidays!.

Pic of the Week

NB – these are the (inflated) opinions of the author, and are NOT investment advice.