My ex-colleage and good friend Ken Leech often recounted that “the story of interest rates is the story of inflation”.

Put differently, where inflation goes determines where interest rates go.

Today, inflation is considered a mystery. Despite the trillions of dollars poured into the US, European and Japanese economies over the past ten years, inflation is yet to be seen. This fact has left central bankers scratching their heads, even US Federal Reserve ex-chair Janet Yellen said it is a “mystery”, a sentiment echoed by new chair Powell.

Furthermore, the obsession with historical relationships like the Phillips curve, and quantitative methods like the “Taylor Rule” seem to offer little insight.

Here we attempt a more qualitative approach, suggesting that inflation is the product of a small number of fundamental driving forces, in much the same way a living cell is the product of complex interacting chemical components known as DNA (deoxyribonucleic acid).

We will show how, in an increasingly globalizing World, it’s little surprise that inflation rates around the World are converging upon one another. Country specific issues play a small but minor part over the cycle. Therefore, throughout the paper we will use the term inflation as pertaining to both US and global inflation trends. We will discuss individual country-specific factors in future posts. Further, we will discuss at a later date, how departures from our model will impact financial variables like fx, and subsequently enhance the country specific issues.

The Four Bases

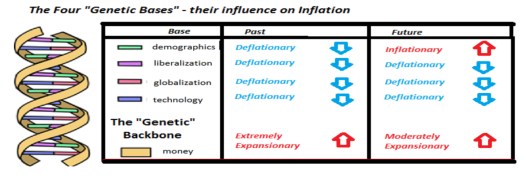

In this paper we suggest that inflation’s “genetic DNA code” also has four fundamental “bases”, and that the path of inflation is determined by how these four major forces interact with one another. Money, and therefore monetary policy, forms the backbone.

We suggest the recent low and stable inflation rates are the result of the deflationary interaction of these four bases or forces:

- Demographics,

- Globalization,

- Technology

- And liberalization

Monetary policy has fought these forces with easy policy, and the result, a low but positive inflation rate.

The Future of Inflation

Here we will contend that the future path of inflation will be dominated by technology – Artificial Intelligence (AI) and robots.

We believe technological advance will mitigate any reversal (aging) of demographics, and as such, inflation (and therefore interest rates) can (and should) remain lower for a lot longer, provided policymakers remain patient.

The Great Moderation – The Mystery of the Missing Deflations

Until 1955 the probability of either inflation or deflation – defined as negative changes in overall price indices – was about 50%. Deflations were very common, and often of significant amplitude (see chart below)

Typically a deflation was precipitated by a society-enhancing technological advance, which seeped through the economy, reducing all prices from commodities to finished goods, and increasing real incomes and wealth. Inflations on the other hand, especially of the more pernicious type, typically resulted from the behavior of governments debasing their currencies after a war.

Note that during the previous globalization episode, 1870 to the outbreak of WW1, deflation was the norm, and inflation was rarely positive (chart above). We’ll revisit this previous phase of globalization later.

By 1950 the deflations simply disappeared, at least until a brief moment during the 2008 crisis.

We believe the recent period of low and stable developed world inflation (Exhibit 1 – inset) was the result of dovish monetary policymaker behavior in the face of the four “bases” – rampant and successful globalization of society, positive demographic forces, technological advances and liberal attitudes to trade, politics and of course finance.

These four mutually reinforcing, inter-woven forces each enhance the power of one another and make up inflation’s “genetic DNA code”. Money, and therefore monetary policy, forms the backbone. No one force “drove inflation” since the 1980s. However all four were pointing in the same (disinflationary) direction. A direction that monetary policy has leaned against, and with success.

We now introduce each of the “bases” in turn, explaining how they impacted inflation since the 1980s. We also explore how they could influence inflation in the future, finding the future will be dominated by technology and demographics.

The Four Genetic bases and their influence on past and future inflation

Demographics – the past

The demographic dividend bestowed upon the world in the 20th century was actually four stories in one – (1) increased life expectancy due to improvements in medicine, (2) the post- WW2 “baby boom” (3) increases in female participation and (4) immigration. The surge in labor forces increased demand, and togther with the oil shocks, set the seeds for the “Great Inflation” of the 1970s. Aggressive monetary tightening fought the inflationary threat, while the “boomers” simply added to the unemployment rate, christening the term “stagflation”. The inflationary consequences were only felt briefly while the boost to the labor force, when combined with globalization, enhanced the pressure on developed country wages. By the 1990s the overall impact was strongly deflationary. The internet and ICT revolutions allowed global multinational corporates take full advantage of the increased labor, and optimize production and global supply chains. The net effect was to increase pressure on wages and reduce inflation.

Demographics – the future

Today, commentators focus on the reversal – the “greying” of societies as mortality continues to improve while birth rates collapse below replacement. The consequent challenges are well flagged, perhaps as far back as 1976, straining pension systems and government and municipal budgets. The impact of this reversing demographic force on inflation will depend upon which solutions are chosen. Conventional wisdom suggests one saves while one works, and spends when one retires, driving demand and increasing inflation. But this era has been the opposite, due to being “under- saved”, and about 35% of US post-retirees return to work. The consequent increase in savings and workforce participation will prove disinflationary. The impact on inflation from such a dramatic reversal in demographics seems uncertain and path dependent, and we instead foresee the forces of globalization and technological advance as the arbiters of future inflation. We’re optimistic they will neutralize any inflationary impact from the reversing demographics.

Liberalization – the past

By liberalization, we mean the many aspects of deregulation and reform, from the financial system to trade arrangements. Liberal attitudes permeated the global psyche offering new ways of doing business. The multinational corporation became a major force in this period.

Liberalization of finance, in its many forms, was essential to the current success of globalization, in particular the modern debt markets and the liberalization of savings systems and ethics, to produce demand for the growing debt. From 401k in the US and pension laws in UK, Australia and Europe, to accounting and regulatory standards, a sophisticated financial system evolved, capable of diversifying risks which were increasing alongside exploding global trade. Liberal attitudes to trade agreements enhanced that trade, while the modern multinational grew to optimize and arbitrage global price and cost differences and resource opportunities. Tax systems struggled to cope, but overall, global commerce permeated low and stable inflation.

Liberalization – the future

Recent events point to setbacks to the liberalization process, especially in trade (US leaving TPP), while the threat from technology has initiated consideration of extreme social programs to alleviate structural unemployment, including Universal Basic Income (UBI). Each of these are likely mildly inflationary in the short term. We are optimistic that renewed liberalization momentum is not far away, centered on global tax policy aimed at incentivizing multinational corporations to invest their huge cash pools in real capital assets, while reducing debt issuance and switching financing towards equity. As regulatory fatigue sets in, improved deregulation can initiate re-leveraging of bank balance sheets further remedying strains on public finances, and reinvigorating entrepreneurial sprits. Meanwhile the “hunt for yield” should ensure continued flow of investment capital and, barring a major financial crisis, sustain market valuations supported by low and stable inflation. Overall, renewed liberalization should support low inflation.

Globalization – the past

Globalization can be defined as the full integration of the world’s resources through commerce, trade, migration and transfer of capital. It has failed in the past, primarily due to the rigidity of the financial system. The abandonment of Bretton Woods in 1971, and the post-oil shock growth in the offshore euro-$ markets allowed this globalization to fully utilize the “vendor financing” method of financing rapid growth in trade. Between 1980 and 2010 a billion low cost non-farm workers were introduced to the global labor market, and multinational corporations were able to optimize location of production and the capital/labor mix to reduce wages and prices. The threat of off-shoring of production reduced global wages while enhancing equalization between developed and developing countries. The recycling of surpluses created by trade, together with liberalization of savings systems fueled essential debt growth, supported by low inflation. The net result was a strong deflationary pressure on wages and inflation.

Globalization – the future

The current phase of globalization has benefited from the flexible monetary order which evolved after the oil shocks, and was enhanced by “vendor-financed trade” alongside the “risk transfer” ethic. This combination created a remarkable self-reinforcing stability in the path of globalization. While globalization of capital has likely reduced costs (and therefore inflation) via supply chain efficiencies, access to working/investment capital, and lower interest rates, it’s this stability that has maintained capital flow and ensured the disinflationary outcome. Described as the infamous “global savings glut”, creditor countries surplus savings are used efficiently to lubricate the globalization process, yielding important gains for all parties, which also reduce the risk of fatigue and setbacks. Recent signs of fatigue, in the form of the growth of populism and trade setbacks, will likely be short lived. Global momentum will likely re-emerge as tax and regulatory reform re- invigorates multinational corporations, fostering higher investment in new technologies and increased optimization of global value chains, adding to disinflationary price pressures in the future.

Technology – the past

So far the direct impact of information technology, in the form of the internet and ICT, has been sizeable but relatively short-lived, as the productivity gains have been absorbed. A more lasting impact is that of price discovery, enhancing the global transmission of disinflationary price pressures – “battlefield radar for commerce” had been invented. The productivity gains in the mid-1990s and early 2000s were substantial and greater in emerging economies, but only when combined with globalization and the innovation of multinational supply processes, can the influence of technology be seen in driving prices and wages down. Technology enhanced global supply chain efficiency while automation enhanced production processes. Through the 1990s, labor’s share of the pie declined steadily and routine employment declined. By the late 1990s the overall impact was strongly deflationary.

Technology – the future

As the positive effects of demographics and globalization decline, it’s now crucial that the new technological wave is allowed to exert its deflationary effects. While threatening full replacement of human labor, what’s more likely is enhanced augmentation, where AI and robotics enhance human labor. In some cases full replacement is likely to occur, and these disruptions will force re-skilling and adaptation, and societies should begin to debate appropriate policy now. The overall impact will be to lower most labor costs, while enhancing the value of the skills technology cannot cost-effectively replace. Meanwhile, technology will generate growth rates of income and output large enough to alleviate the current debt loads while supporting general asset valuations. Developed nations will re-emerge as the winners, but emerging nations will benefit from increased efficiencies in production of commodities. Work itself will be transformed, and overall, deflationary price pressures will grow significantly over time.

Explaining the “Great Inflation” of the 1970s

The period of very high inflation at the end of the 1970s is a good example of how these forces, or bases, interact to change the “polarity” of one another.

Beginning with the sharp increase in female participation in the 1950s, by 1970 the first baby boomers were entering the workforce. Taken alone, such a sharp increase in the global labor force through the 1960s and into the 1970s, would normally have had a meaningful impact on consumption of resources (larger), economic growth (stronger) and prices and inflation (higher). Furthermore, monetary policy was in its infancy, especially the understanding of (and accounting for) money. History records that policy was too easy at a crucial time, as the “resource wave” hit, and in the end, all that was needed was a spark. This inevitably came in the form of the commodity price shocks of the late 1960s, culminating in the 1973 oil shock. Before policy could be tightened sufficiently, a second oil shock hit in 1979, exacerbating the already inflationary consequences of the pre-1980 demographic wave (see chart below).

When monetary policy was aggressively tightened to meet the inflationary threat, the arriving “boomers” simply added to the unemployment rate, christening the term “stagflation”.

The inflationary consequences were only felt for a short while during the 1970s. The boost to the domestic labor force, when combined with freshly enhanced globalization, increased the pressure on developed country wages, and by the 1990s globalization and liberalization were ascendant, resulting in strongly deflationary forces.

As we discuss in detail later, once the globalization kicked up a gear with China’s entry in the early 1990s the ‘boomers” were already at peak earning and spending power. The ICT (information, communication and technology) revolution was also well underway, helping global multinational corporates develop super-efficient global supply chains and improving price visibility at the consumer level. The net effect on inflation, at least from the 1990s, became more and more deflationary, and required ever easier monetary (and fiscal) policy. It was during this “NICE” period, [1] that central banks gained the bulk of their credibility, and adopted “inflation targeting” as a formal policy.

Footnote [1] – BoE Governor Mervyn King christened the period – “non-inflationary consistently expansionary – or “NICE” – a decade in which growth was a little above trend, unemployment fell steadily, and, supported by the improved terms of trade, real take-home pay rose without adding to employers’ costs, thus allowing consumption to grow at above trend rates without putting upward pressure on inflation.”

The Future of Inflation – the Conflict between Demographics and Technology

In this paper we described the four fundamental “genetic bases” of inflation;

- Demographics,

- Economic and financial Liberalization

- Globalization

- Technology

We also described how they have interacted to determine the recent path for inflation.

Somewhere in the 1970s, all four forces turned deflationary, and in so doing, acted to;

- reduce global costs,

- pressure developed world wages,

- break unionized labor,

- drive global goods and service inflation down,

- reduce asset risk premia,

- drive global asset prices up.

As a result, global central banks acted to align monetary policy against these deflationary forces, preventing deflation, but at the cost of occasional financial crises, high public and private debt levels, and rising inequality.

The post-war increase in population, rather than providing a durable increase in demand and inflation, instead rapidly provided the raw material for globalization to relax productive capacity constraints, resulting in strong global growth and increasingly deflationary forces. As globalization took hold around the 1980s, the demographic dividends of the baby boom and falling mortality, alongside the liberalization of finance and trade, combined to create strong deflationary forces which monetary policymakers prudently pushed against via easy monetary policy. The evolution of a flexible financial system, finally able to exploit the benefits of fiat money, utilized vendor financing and risk transfer to generate rapid but mutually stabilizing growth in trade and debt. This however came at a cost – financial crises triggered by speculative financial excesses which exposed the inherent weakness of this new “dollar standard” – collateral.

But without doubt, the global debt super cycle is the direct result of the successful globalization. Global trade was financed by debt through vendor financing and risk transfer, enhanced by liberalization of finance and commerce culminating in the offshore Euro-US$ Libor markets.

Which brings us to today. We now face the reversal of the demographic force and commentators are rightly questioning whether this portends significant increases in interest rates and inflation.

Meanwhile globalization is suffering from significant fatigue, although we anticipate this being temporary, and in time, expect this “base” to revert to it’s deflationary norm.

Crucially, we envisage technology stepping into this breach, eventually providing deflationary forces that more than compensate for the waning demographic benefits.

Meanwhile we see little reversal in finance and commerce, and can imagine multinationals, freshly incentivized by the tax reform, to utilize offshore cash pools to finance their participation in the coming technology boom, even in the face of some reversal in trade liberalization.

So the future of inflation will be determined by the battle between the increasingly metallic technology and the rapidly graying demography.

As a result, the key consideration remains –

The story of interest rates, especially central bank policy rates, is still the story of inflation.

Paul, didn’t know this was here and enjoyed reading the DNA article. Frances Coppola and I corresponded on this, specifically demographics and inflation- why did inflation exist in the 70s (boomers) and not in the naughties/now (China). Impossible to find twitter threads and I can’t remember the article/twitter that started the dialogue. Entirely different, what do you think of New Yorker/Bannon? Best

Drew

LikeLiked by 1 person

thanks Drew. I plan further articles to flesh it out. But the premise is that technology is the key to low and stable inflation, if not outright deflation.

Bannon is an interesting topic – watch this space

LikeLike

I got what you mean ,saved to favorites, very nice internet site.

LikeLike

Loving the info on this site, you have done great job on the posts.

LikeLike

I enjoy your piece of work, appreciate it for all the useful posts.

LikeLike