- Markets always have many things to worry about – some known knowns, some unknown knowns, even some known unknowns. However it’s always the unknown unknowns that really kill.Right now in the known unknowns camp, we might put inflation (is it finally going to bark?) and monetary policy (will global easing turn to global tightening?).Both are topical, and worrisome to markets, but here, I’ll argue that neither are serious worries, though the worry they are both causing, especially when combined, was the real reason for the current market turbulence.

In Summary

This note will argue that;

1 this was a healthy correction

2 the validity of market valuations hasn’t changed

3 the inflation scare is just that, a scare

4 the tinder for the fire was the VIX derivative positioning, esp XIV

5 the match that lit the fire was last Friday’s wage data,

6 but in the context of the Ecb taper noises and the Mnuchin “weak dollar” threat – akin to the Baker-German spat in 1987

7 we can relax a little more on the threat of machines blowing up the system

8 but market liquidity remains a problem and was largely untested

9 while the potential dangers inherent in ETFs are on people’s lips

10 as is risk parity again, and we recall the 2013 Fed Taper Tantrum

Main report

Markets always have many things to worry about – some known knowns, some unknown knowns, even some known unknowns. However it’s always the unknown unknowns that really get ya.

Right now in the known unknowns camp, we might put inflation (is it finally going to bark?) and monetary policy (will global easing policy turn to global tightening?).

Both are topical, and worrisome to markets, but here, I’ll argue that neither are serious worries, though the worry they are both causing, especially when combined, was the real reason for the current market turbulence.

Un-easing? Surely you mean monetary tightening?

Why do I refer to monetary un-easing? Well, I find it hard to consider the current moves by the Fed, let alone possible moves by the ECB and BoJ as actual tightening. They remain within a whisker of emergency policy settings, with rates close to zero or negative, and balance sheets well and truly bloated (and in some cases growing). Monetary policy remains “foot to the metal” – and that is precisely why financial conditions remain very easy. Indeed throughout the Fed’s rate hiking cycle financial conditions have tended to ease further.

So as the Fed hikes, it’s analogous to lifting one’s foot off the accelerator pedal, NOT hitting the brake! Indeed, think changing gears when considering central bank balance sheet manoeuvres and the driving analogy is complete. Un-easing.

How far to Tipperary? No idea but I wouldn’t start from here.

There is never just one cause when it comes to market turbulence of this order, just as there is never one father to a profit (though losses are always born parentless for some inexplicable reason). And so it is this time.

One reason will inevitably be the location of markets and the state of global politics. Both feel “as good as it gets” and it’s easy to see grey clouds on the horizon. And yet they never seem to rain. We always seem to be in a state, reminiscent of that wonderful joke about a tourist asking an Irishman how to get to Tipperary – “I’ve no idea, but I surely wudn’ start from here”. But here we are.

There are many reasons why markets were where they were mid-January, and most are well trodden, though I suspect the real political and fiscal policy effects of the US Tax Bill, and more importantly the next “Shakespeare play”, Infrastructure [1] have yet to be fully priced. Valuations could be too low after all.

So let’s imagine for a moment, we all know the “how we got here”.

And let’s recognize that, as an analyst on Bloomberg said on Monday “we expected a correction, but not from this point exactly”.

So we’re left with one question – WHY?… why now, why here, why in this form? It doesn’t matter how you pose it, it’s the SAME question.

Haven’t I seen this movie before?

How about this for a simple, “focus on the few not the many”, raison d’être?

Through January, various ECB governors talked confidently (again) about their desire to end their QE program (having already tapered it a little).

That left us with the reassurance that the ECB would continue to buy (or reinvest) along with the BoJ and the Fed, many trillions more (mainly) government bonds.

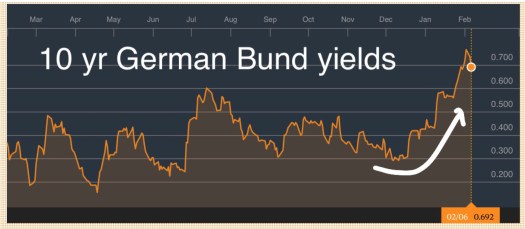

But where’s the gripe? – it can’t be that they actually might do it, since they’d cried wolf many times before and nothing like this happened to markets. However, German Bund yields took note and have doubled since early December (chart), matching the sharp rise in US Treasuries almost one for one.

Source Bloomberg

Source Bloomberg

Furthermore, adding to the overall cautious sentiment, the BoJ have privately hinted they might be keen to change their monetary policy settings, perhaps moving their bond yield target (and their purchases) down to 5yr maturities from 10yr, allowing a steeper yield curve to help their banks.

Then on Jan 24th, at wintery Davos, USTS Mnuchin made what to many of us felt like the first “soft dollar policy statement” in many decades.

Essentially he was saying to the Europeans (and ECB) “if you want to tighten, go ahead, we’d love a weaker dollar” – aka a Euro headed to the moon…

For those of us old grey history buffs, that phrase resonated with Baker’s fight with the Germans in 1987 (I explain more below).

But for the remaining 99% of marketeers, it simply said “easier financial conditions, at a time when inflation is picking up, and the Fed is 3-choice on hikes while the market is 2-bid at 3 – oh oh”

The immediate sell off in US treasuries and the dollar was enough to start the rot.

Add in a firm payrolls, sprinkle a pinch of wage inflation (oh please…) and voila…

Manic Monday…

A pale shadow of Black Monday just over 30 yrs ago. but never the less a shocker.

So where does that leave us? What should we look to for as a reverse-canary all clear?

Well, apart from German Bund yields, which will determine whether we should believe the inevitable back tracking of the ECB now they’ve upended markets, the other canary has to be the Fed.

What’s Jay Sayin’?

Having used the phrase “Fed’s Yellen out loud” more times than I can remember, we have to move on – and perhaps the new phrase will be “What’s Jay Sayin’?” referring to Jay Powell the new Fed Commander in Chief.

So what is he even thinking? Barely confirmed, he faced a first week on the job that would rival that of Will Smith in “Men In Black”. But he shouldn’t have been surprised given the similarity today bears to the backdrop a previous new incumbent faced back in the summer of 1987 – a new Fed Chair – G7 intrigue between US Treasury Secretary Baker and the Germans – trade wars with Japan – rise of machine-based trading & portfolio insurance – and of course inflation picking up from recent 20yr lows – see chart).

I’d strongly recommend Jay Powell read Steven Beckner’s excellent book “Back from the Brink “ especially pp 39-66. That summer, Greenspan was thrown into the G7 mess head first, facing Black Monday on Oct 19th 1987, where stocks fell 20+% in a day, led by mechanised hedging (portfolio insurance), and needing to react fast. He famously “hit the ground running” and the rest is history. Let’s hope Jay has a copy of Beckner’s book to hand.

But either way, the idea that this market correction, as it surely will turn out to have been, will help to temper both the Fed’s and the market’s enthusiasm for faster “un-easing” of monetary policy, is very unlikely. In a word, the “3 choice” for 2018 hikes could begin to look more like “2 bid at 3”. But no more. Indeed Thursday’s comments from (retiring) NYFed’s Dudley made it pretty clear these are “small potatoes” and even 4 hikes are a possibility this year, as is just one hike.

Then of course, there is the age old question of the “put”.

Will Jay put the “put” in writing?

In short: no. There is unlikely to be any need, at least based upon this pro-growth, inflation-stirring, hedging-frenzy, market correction.

But depending upon how the geo-political and geo-monetary co-ordination goes over the next few years, I’d expect the market to become familiar with the “strikes” of the “put” that this new, Jay Powell Fed has in mind.

Machination of the Machines

While staying with reality, we have to ask, what part did the “machines” really play this week?

Well firstly ETFs clearly played their part, with their algorithmic hedging processes, and many point to the stronger price performance of the stocks less represented in the big ETFs as evidence. Let’s concede that one.

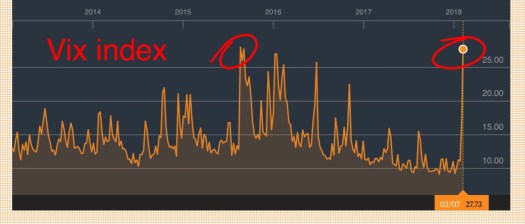

More important is the part played by the algos which trade volatility, especially those tied to the VIX, and most notably the XIV ETN, which (who knew) few knew contained a nasty knock-out put that the issuer CSFB could choose to exercise if the VIX had one of those days it has never had… and low and behold they did exercise – they “accelerated” the maturity of the note paying it’s value, now almost zero.

On Friday the 666pt Dow fall [2] was enough to initiate a sharp rise in the VIX which left the short-VIX traders needing to buy over 200,000 VIX futures, after the close, in the after market. This would be big volume in normal hours, but as it’s a hedge they executed with vigour, driving the VIX index through the roof. The buying of the VIX futures led to enormous follow on selling of SP500 futures, as the hedging of one instrument passes onto the risk of another derivative trader, and asset.

The good news is this was all done efficiently by algos and is our first real test of the machine-traded markets we’re heading head first into…

The impact on stock markets was devastating, and this was the main reason Monday was so manic. But with the bulk of the emergency Vix hedging done, and almost half of the approx $8bil short-volatility-based ETP and ETN exposure wiped out, any enthusiasm for buying VIX above 40 (having traded at 50) was left to those who needed to say “we did something”.

Little surprise that VIX has collapsed back to half it’s high, resting around the highs it got to in the last panic in 2015, allowing genuine hedging and stop losing to take place, as the chart shows.

Source Bloomberg

Source Bloomberg

In a nutshell, the VIX-based panic is over, though some further hedging is likely and markets are now vulnerable to any bad news.

The investors in XIV and such-like products will have done their homework (hopefully) and have been fully aware that these products were not designed for retail, not designed to be “held to maturity” and thankfully too small (at about $4bn) to have a meaningful impact on the financial system and economy. The much-maligned regulators can feel good about this one.

So is there an inflation wolf at the door?

No.

The plain fact is that inflation has been the wolf that hasn’t even shown up, let alone barked. And for very good reason. In a future post [3] I’ll examine why it’s been benign for so long, and more importantly why it’s very unlikely to show up any time soon. We remain in a secular disinflationary environment requiring an easy global monetary setting to prevent deflation.

However in the short run, which is where the market’s mind (and it’s anxiety) is firmly located, inflation is set to look “strong”.

Many private forecasters expect US CPI to move up towards 3% by late summer, a forecast I have no problem with at all. That of course means (based upon the well known “wedge” of about 0.5% between CPI and the Fed’s preferred target measure the headline PCE deflator) the Fed will finally “hit” her inflation target for the first time in years, at least for several months[4] (see chart).

Coupled with respectable readings on other inflation measures like Wages (ECI and past Friday’s average earnings) and of course unit labor costs, the tone is once again (as it seems to be every “new year”) one of “inflationista” – the wolf is at the door.

Given I expect this to remain the case into the late summer, the machinations of the global central banks will be crucial to the risk-taking environment.

While I personally doubt any of the major central banks will risk much angst, I would expect their regular desire to “scratch the itch” to initiate regular bouts of volatility in markets.

It’s going to be a busy, “volatile” summer.

So where does that leave us?

Well first there’s the good news;

The markets came through their first real “fire alarm test” of the Trump era.

They also showed that (maybe) some of the fear that a machine-dominated, ETF-based financial market would explode into a series of “flash crashes” that destroyed the system itself, is overblown.

It was clearly a case that algo-based trading dominated the “focus” stressed markets (VIX and stocks) and yet we didn’t even trouble the circuit breakers.

Finally, concerns that stocks are bubbles, like Bitcoin, with the same fate waiting, devoid of fundamentals and driven by FOMO intent[5], also look overblown. Indeed, based upon the media and TV, most “pundits” still saw the potential in 17-PE stocks and corporate bond yields supported by very low rates and a “gentle Fed”.

In summary, this was one of the cheapest “lessons” markets could have suffered, and yet, it may yet have a healthy impact on markets – yes they can go down fast, and yes, they are always subject to volatility, more so when they’ve been so becalmed for so long. Caveat Emptor.

Then there is the inevitable not-so-good news;

Firstly there is the damage to the market psychology. It’s likely now aware that inflation is on the rise, at least for the short term, and that policy makers are itching to remove some of the emergency policy, either in the form of higher rates or smaller balance sheet (or in the case of the Fed, both). Secondly, the recent spat between the US Treasury and the ECB, though subliminally registered by markets, reminds us that any policy reversal is bound by the rules of the Prisoner’s dilemma,[6] and requires immense co-ordination – there is a “Game of Bonds” afoot, and one players’ pre-emptive moves surely influences the latitude of the others to act.

More worryingly, one wonders if these questions have been sufficiently posed;

Firstly, was market liquidity tested, and in which markets, and to what satisfaction?

Plainly, the stock market index futures (and even the VIX) performed admirably. But many markets seem to have been bystanders. Imagine if market participants felt market liquidity was already (normally) poor. Seeing these events, the temptation might be to do nothing – see how it plays out. Indeed it may have been seen as futile to try to move large exposures in many markets.

While dealers will naturally widen bid-offer spreads to protect against large flows in either direction, the fact that no one bothers to do much “asking” means mid-prices don’t move. With prices unchanged, there is rightly nothing to do. And order is preserved. Some might call this the “circle of stability”. Others might be more unkind.

Secondly, a major investment thesis has once again been thoroughly tested – the concept of “risk parity”[7]. While short vol strategies probably amounted to no more than $8-10bn, risk parity, which is also sensitive to vol, is thought to be around $600bn. Indeed, many investment styles, including those in fixed income, parody the risk parity methodology without the technical rigor. As we saw in 2013, the Fed’s “Taper Tantrum” phase sorely tested these strategies through out the summer. If we’re right about our views on inflation, policy uncertainty, and markets, we could be in for a similar test.

Thirdly, volatility itself. Like inflation, the word volatility is also often misinterpreted – it means something different to everyone. There are different measures, different periods of measurement, and different uses by different market practitioners.

All of the discussion this week has seemed to discuss “implied volatility” – that number implicit in market prices, be they options, or volatility indices like the VIX itself.

Ask yourself, how often have you heard a discussion of realized volatility? Would you know what it’s actually been over the past 1 month? 3 months? 10 yrs? Is it that remarkable?

It’s plain that 2017 was special for it’s “calmness” – barely a 1% daily move in major stock indices all year, and a market that largely went up in a (slightly curved) straight line.

So a 5% move in either direction, helps restore some “average” normality.

Indeed, as the chart below shows, even with this weeks’ behaviour included, the past 3 months have barely matched the average volatility of sp500 prices over the past 8yrs.

It’s the realized price action, not the implied, expected volatility (implicit in markets like the VIX index) that actually matters. If markets fail to be as volatile, then buying hedges and protection at these still very high levels of implied volatility will prove very expensive. One has to expect a lot more weeks like this one, even over the next 3 months, to make the current “price of volatility” a good investment.

Source S&P Indices.

Source S&P Indices.

Notes

[1] I have viewed the new US Administration through three simple lenses;

- The White noise – eg the tweets, the speeches, the rants, mainly by POTUS

- The Kabuki theatre – the stuff that goes on behind the curtain – we see the shadow and think we understand, but it’s largely misdirection for a political aim – to succeed with the final one. The real policy “play”.

- The Shakespeare play – the main agenda – what the administration wants to get done – and usually it requires a mix of a) and b) to “out” the opposition, tire them in front of the media, and watch them wilt.

[2] a pretty meaningless % fall, but why mkts talk about Dow points, the devil if I know…

[3] “Cracking the Genetic Code of Inflation – the future is metallic silver”

[4] We can’t really count the 2 month success back a year ago, as it was so short lived. This time we can expect them to be at or above 2% headline PCE for at least 6 months, during which of course, most will extrapolate inflation higher.

[5] FOMO – Fear Of Missing Out, a phrase I have often used to describe the perfectly natural market instinct in a world of diminishing (asset) return and ever greater need to defease (liabilities).

[6] https://en.wikipedia.org/wiki/Prisoner%27s_dilemma

[7] Perhaps the best explanation is here https://www.bridgewater.com/resources/all-weather-story.pdf

3 Replies to “Markets have an uneasy feeling about uneasing.”