Markets have been taking center stage since the vol-ruption nearly a year ago, and while realized volatility has indeed increased alongside implied, options markets Vix-volatility, many have taken this to mean the end is nigh and all manner of skies are about to fall. This may be true, but there is another, orthogonal perspective which we describe here. As it’s always best to cycle with a friend, we will be joined by Ed Casey on this tour de cycles.

Is it the end of the World as we know it?

Back in November last year, while noting that for all the fuss about bubbles of bubbles, stocks had gone nowhere, we wrote

“This may be end of credit cycle/turning point stuff for sure.

Then again it may not be – there are plenty of examples in history of such markets, where the highs in broad stocks are resumed after a period of chopping and starting.

Whether this is one or other will be determined by events, the outcome of which no one can know for certain right now,”

Well, apart from the December “blood bucket” (i.e. less than a bath, more than a cupful) we doubt there is any better indication as to the answer to that question. Indeed we feel policy makers “get it”, and are now in more control of markets – they have their attention, and therefore can iron-out the “bend in the cycle” that we’re fast approaching.

In what follows, we will attempt to assess the facts of the current situation, and even some “fundamentals” on the credit markets, offering an unemotional conclusion perspective on the what the year might bring.

Are we dead yet dad?

In the Long Run we’re all dead, or so JM Keynes would have us believe. So, to for credit cycles. But do credit cycles die of old age, in some pre-ordained manner? Or are they hit by the proverbial bus. And of course, is that bus always driven by the Fed?

If there was one simple fundamental that has initiated many credit shocks, and ended many a credit and economic cycle, it’s inflation. And we still can’t see any, and think the policy makers can see even less than we can.

In the following short note, our friend Ed Casey will distil the important factors which have brought us to where we are today in credit markets. Ed has over 15 years of experience in traditional and alternative investing, during which he led the high yield portfolio group at NTAM and a short only credit hedge fund seeded by Julian Robertson of Tiger Management. He’s our go-to guy on credit.

Ed’s analysis will be brief (unlike 90% of bank and broker research) honest, and unbridled (unlike the majority of position-justifying “thought leadership” from the investment community).

The Outlook for Credit in 2019

As we begin 2019, we think the outlook for a continued challenging economic environment and elevated volatility will lead to further dislocations in credit markets. Issuers face slowing sales growth, margin pressure from rising labor costs and tightening financial conditions. Monetary policy normalization and the dissipating fiscal stimulus will degrade credit metrics. Those issuers with greater exposure to floating rate funding requirements will be first to experience worsening interest coverage. These higher uncertainties will demand higher risk premiums when deploying capital.

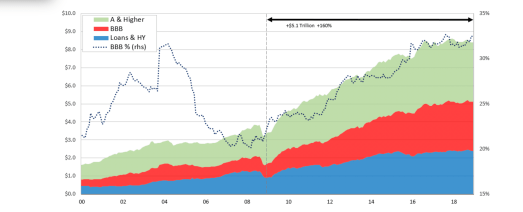

US investment grade, leveraged loan and high yield markets have grown by $5.1 trillion in the last decade. But this 160% growth was not evenly distributed by quality, as BBB exposure increased from 21% to 33%. While loans and high yield percentage remained largely unchanged at 28%, the increase in BBB came from higher quality investment grade shrinking from 50% to 39%. Spread valuations warrant caution as they remain expensive when adjusted for this underlying deterioration in credit quality.

Downturns have a history of following significant ratings migration. With $2.7 trillion of investment grade debt rated BBB, the next downturn could produce between $150 and $300 billion annually of fallen angel debt from investment grade into high yield indices. The vulnerability of passive strategies exposed to those industries which levered up and issued more debt will be an excellent opportunity for active managers to outperform.

Credit spreads tend to move sideways in the final year of an expansion. This presents an opportunity to overweight sectors that are less cyclical, asset rich with defensive and less volatile cash flow profiles. However, spreads tend to quickly widen ahead of and during the early months of economic downturns. Focus on those issuers that can generate significant free cash flow, have business models that provides a competitive edge, that can maintain a feasible capital structure, and provide downside protection via covenants to better survive downturns.

The credit spread thermometer readings, for investment grade and high yield, remain below the average range of the last three economic slowdowns.

However, valuations tied to the highest part of corporate credit capital structures, the leveraged loan market, have gapped to levels consistent with prior recession ranges. This is a cause for concern as we begin 2019. If investment grade and high yield were to experience a similar range move, their valuations would be +22 bps and +87 bps wider respectively from here.

However, valuations tied to the highest part of corporate credit capital structures, the leveraged loan market, have gapped to levels consistent with prior recession ranges. This is a cause for concern as we begin 2019. If investment grade and high yield were to experience a similar range move, their valuations would be +22 bps and +87 bps wider respectively from here.

The challenge going forward is to design credit portfolios to dampen negative price movements. Today’s starting yields are around 4% for investment grade and 7% for leveraged loans and high yield. Although these yields are 50% more than a few years back, the question for 2019 is whether this yield carry offers enough of a cushion to compensate for an uptick in default probabilities or further widening in credit spreads.

In examining historical spread movements (ignoring yield carry and losses given defaults), we see the potential return spectrum is asymmetrically skewed to the downside. Spread widening for higher quality investment grade and leveraged loans into ranges experienced during prior downturns, would lead to further losses of 7% to 10%. For riskier high yields assets, the severity is considerable higher. Under these spread scenarios, the credit yield carry isn’t enough to avoid negative returns. In addition, higher defaults could contribute further losses of 2.5% to 5% for riskier assets. An important consideration for leveraged loans is that a third of today’s yield carry is from higher LIBOR rates, which is at risk of disappearing if we were to experience a reversal in monetary policy.

The Road ahead is full of potholes – wear a helmet.

Today investors should be focused on ways to reduce volatility in their portfolios as timing the exact turn in the cycle is notoriously difficult. Managing credit risk and minimizing exposure to deteriorating and defaulted credits will be the key driver of out-performance. For more traditional credit strategies, having less credit beta and more cash is warranted. For those investors preoccupied with long/short credit strategies, deploying capital to long volatility tail hedges can reduce drawdown risk. For all investors having patience, access to liquidity and being nimble will be key to exploiting the opportunities in the year ahead.

The new environment is fertile ground for active strategies that focus on intensive bottom-up company and security selection.

All in all, we’re likely in a bend in the road rather than the formal end of the cycle.

If you’d like to get on Ed’s list for his monthly credit opinions, contact him via LinkedIn. www.linkedin.com/in/edwardjcasey

And please note, these are all just Inflated Opinions of the authors. hey should not knowingly be construed as investment advice.

One Reply to “”